Amanda and I work in the Buford are KW office. And, we have constantly heard other agents RAVE about this place. I think I had a sandwich from this place a couple years back and it was good, but we just hadn't sought this place out. It is a little off our beaten path.

Well, we were missing out! The first thing that you will notice is that the restaurant is actually a converted service station. It is decorated tastefully.... if Yoda on a shelf with lights projected above it to give a water-like illusion on the ceiling can be tasteful.... When I write that, it sounds tacky... but somehow it worked. One of the other things that worked was the wait staff. Kelly was our waitress and she was fantastic. Not only was she friendly and attentive, she actually knew the specials, and could describe them. She knew the regular menu equally well. She was able to answer questions and give suggestions. Honestly, it was one of the most pleasant experiences we have had with wait staff in at least a day. (There is a certain other place in downtown Buford that we learned not to go for lunch at around 2:15pm. Apparently, their kitchen closes at 2:30pm, and they do not appreciate having people pop in so close to the kitchen closing down) Actually, she really was fantastic and her knowledge of the menu really was amazing. And, she may have been faking it, but we didn't get "I don't know, I've never had that". So, what about the food? Amanda had the Scallop Po Boy special paired with sweet potato fries, and I had the Royal rooster with Fried Green tomatoes. The portions were more than ample, which is saying something because, well.... I am more than ample..... which means I can usually finish my meal. I was unable to today. It was all fantastic. I am a fried food connoisseur. One of the things that bothers me the most is food prepared in old grease, or grease that has been burnt, or that is not kept hot enough. All of our food was fried. (yep.... we are health nuts) And, all of it was delicious. None of the fried foods tasted like they were prepared in old oil and even though Rico's has a lot of fish items on the menu, the Chick, Tomatoes and Sweet Potato chips didn't have any hint of a fishy taste. Everything was crispy, hot and juicy and very well seasoned. And, as far as prices go, it is very reasonable. Mine was under 10.00 and Amanda's was 11.50. If you are looking for a great place that isn't the same ole' same ole', that is delicious, fun and reasonably priced, I hope you will consider Rico's World Kitchen. It will certainly be on our rotation from now on. Oh, and don't forget to ask for Kelly..... did I mention she was amazing?  As I was driving into the office today, I heard a national mortgage company advertising lender paid mortgage insurance, and I thought about how misleading the ad was to the public.

So, here is an overview of mortgage insurance. What is mortgage insurance? Basically, mortgage insurance protects the lender if you default on your loan. It is not home owner's insurance in any way, and really offers the home owner no protection at all. For a conventional loan, it is not required if you are putting down 20%. For an FHA loan, the MI is always required. And, for conventional loans, it is actually Private Mortgage Insurance, which is why it is abbreviated as PMI. For FHA and USDA, it is just MI. PMI and MI can vary in terms of cost due to the following factors: Loan type, Loan Amount, LTV, and credit score. PMI can be removed after a minimum of two years if the loan to value hits 78%. That can happen from additional principle payments or appreciation. Either way, you will likely have to have an appraisal from the banks approved list of appraisers. In fact, they will most likely order the appraisal themselves. You will also have had to have on time payments for at least 24 months. One hitch with FHA loans is that the MI cannot be removed.....ever. This is a recent change, that is often misunderstood. So, what's with lender paid PMI? The lender makes the interest rate higher to pay for the PMI. It will usually result in a lower payment versus a payment with normal PMI. The hitch comes in that your rate will be locked in higher. So, if you were to keep the loan for the full 30 years, you would actually pay more than if you had PMI that could be removed. The point is that the lender isn't paying it for you out of the goodness of their heart. You pay a higher rate. It may be worth it. You may be able to afford a larger, nicer, more expensive home with lender paid MI. But, just know going into it that there are pluses and minuses to this loan product. If you have questions, don't hesitate to call me at 678-992-3817. If you have feedback, please leave it below! And, as always, "Make the Wise Move".  Obviously, as Real Estate professionals, one of the most frequent questions we get asked is: How are the schools? Surprisingly, we aren't allowed to discuss the quality, or competence of the schools. I know this sounds absurd, but it is true. In some ways, this is good. Everyone's standards differ and what is a good school to me, may not meet your criteria of a good school. I encourage all of my clients to do their own homework.

First and foremost, unlike a decade ago, there is an abundance of information about schools on the internet. Here are a list of websites that can help with your initial search. ' Great Schools This is great first step. You can search for any school district that you are considering to see how it ranks. It will rank schools on a numerical scale from 1-10. School Digger This website begins to give you a little deeper statistical analysis of how the schools rank. Niche Rankings This is a yearly ranking by Niche. This is based on several different statistics as well as reviews from students. U.S. News ranking of High Schools in Georgia. And, finally, this is a ranking is by U.S News. This is based on four key metrics listed on the website. What next? All children and all parents are not the same. So, a great school for one student and parent may not be a great fit for another. Pay attention to things like student-teacher ratios, or whether a school offers a specific program that engages something that you child loves. Some schools have video, photography, or broadcasting classes. The key is to find the school that is right for your child. If you are seriously considering a home, head to the neighborhood when school lets out, and talk to some of the parents. Head to the school and talk with the principle and ask for a tour. Walking through the school will give you a first hand look at what your child will see everyday. And, finally, remember, that regardless of the schools ranking, the success of your particular student can be directly influenced by your involvement, and your student's hard work. Please feel free to reach out to me with any suggestions or feedback that you may have. You may already know all this information, but I run into a lot of clients that have questions about this. Figured I would get it right from the horse's mouth.

By Keith Loria

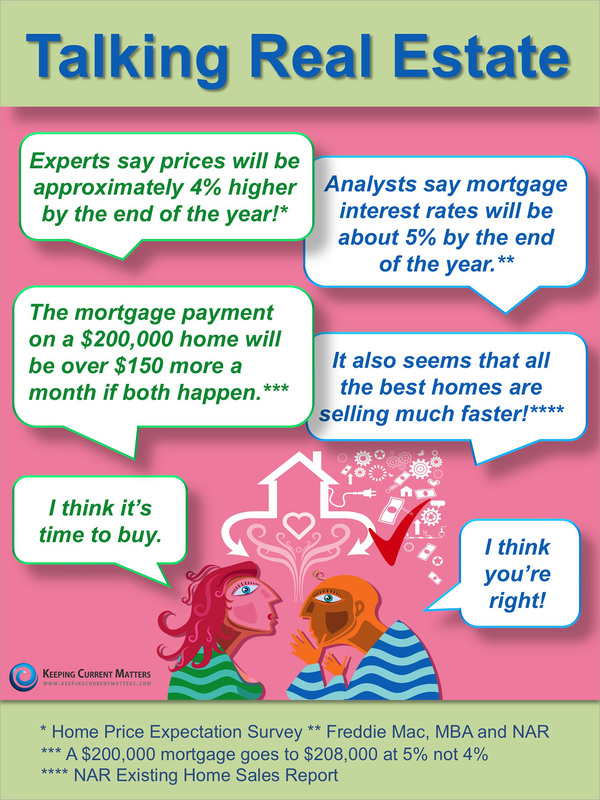

Our military personnel do a great deal for our country, and one of the ways the government thanks them for their service is with the VA loan program, which allows both past and current military personnel a better option for financing. Originally established in 1944 as part of the Servicemen’s Readjustment Act, a VA loan is available for any individual who has served in active duty in any branch of the U.S. military for a minimum of 90 days, and it has helped millions of people and their families purchase a home. In addition to servicemen and servicewoman, non-active duty personnel, such as individuals in the Army Reserves or National Guard, may apply for a VA-backed mortgage, provided they have completed six years of service. The spouses of deceased or missing military members are also eligible if they have not remarried. The major advantage of a VA loan is that it doesn’t require a down payment. It also doesn’t have private mortgage insurance. It does require the borrower to pay a one-time funding fee on their purchase, which can be paid up front or financed into the total cost of the loan. The funding fee for regular military members is 2.15 percent of the loan. Reservists pay a fee of 2.40 percent. According to recent figures by the Department of Veteran’s Affairs, more people took advantage of the program in 2013 than ever before, with close to 630,000 VA loans given out. This was mostly due to historically low interest rates. Still, many veterans, especially those discharged years ago, often don’t realize that such a benefit exists. That’s why the Department of Veteran’s Affairs has increased its efforts to let veterans know about the VA loan program, and all the benefits it offers. To qualify, borrowers must show enough monthly income after paying personal debts and housing costs to meet “residual income” levels set by the department. A VA loan must be for a primary residence and the limits on the amount someone can get are based on area median home prices. The 2014 limits range from $417,500 to $1,094,625. One other important note: borrowers who received a dishonorable discharge from any military branch are not eligible. To learn more about the VA loan program, contact our office today. Reprinted with permission from RISMedia. ©2014. All rights reserved. In Trulia’s 2014 Rent vs. Buy Report, they explained that home ownership remains cheaper than renting throughout the 100 largest metro areas in the United States; ranging from an average of 5% in Honolulu, all the way to 66% in Detroit, and 38% Nationwide!

click here for other interesting details from Trulia's report.  Edited 10/01/2013- I was dead wrong yesterday.

Well, no matter which side of the isle you are on, the government shutdown could affect you. As far as Real Estate transactions go.... this is a big deal. President Obama said specifically that "Federal loans for rural communities, small business owners, families buying a home will be frozen," Yesterday, I went into each of the loan products and what the impact would be. Well, if you aren't already in process, there will be significant delays regardless of the loan product. Mortgage companies use a system to verify SSN's and another system to verify tax returns/income. These systems are obviously run by the IRS. And, these systems are currently shut down. Until the government is started back up, cash offers should carry even more weight than normal.  Wrong. This is one of the things that buyers often struggle with, but the seller has no obligation to fix the property or to reduce the price.

The due diligence period, or inspection period, depending on the contract, merely affords you the opportunity to have the home inspected. There is no obligation on the seller's part to complete repairs or reduce the price in lieu of repairs. Once the inspection is complete, you can ask that the seller complete repairs. At that point, it becomes a negotiation. They may elect to fix everything you ask for, or NOTHING you ask for. There are many things that affect the seller's decision. #1) Market- If the market is a seller's market, (as it is right now in our area), the seller knows that even if you don't complete the purchase, someone else is right behind you bringing another contract. Now, conversely, two years ago, sellers just wanted to hold the contract together, so they would fix just about anything they could. #2) Financial ability- Some sellers have no money to pay for repairs, or financial flexibility to reduce the price. #3) Types of repairs- Is it a safety issue? Is it a functional issue? If so, many times, these get fixed. But, the reality is that if you are buying an existing home, and not one that is being built, there will be some minor things that the inspector can find. Even on well maintained homes. So be reasonable with what you are asking. #4) Seller's perception of your original offer- If the contract price is really lower than they wanted to go, and they feel like you are getting a 'steal' to begin with, they will be less likely to complete repairs. #5) Motivation- The market plays into this as well. However, if a seller is being transferred, or has another home under contract, or is getting a divorce, or..... fill in any scenario in which the seller has pressure to get the sale completed, then they will often agree to far more repairs in order to keep the contract and sale moving forward. #6) Type of loan- Some loans like FHA, VA, and USDA all have minimum property standards. If the inspector finds something 'should' come up when the property is appraised by the bank, then the listing agent should advise the seller to go ahead and get it fixed to keep it from being an appraisal/lending condition. #7) How long has the home been on the market- This goes into motivation as well. If the home was on the market for a week, then the seller may just elect to put it back on the market and get a buyer that is less picky. Heck, maybe one that doesn't even get an inspection. If the home has been on the market for a year, then they will be motivated to keep the sale moving forward.... of course, unless they just don't have the financial capability. I have it posted elsewhere, but you should ALWAYS get a home inspection. When you fall for a home, it is often like the beginning of a romance..... there are flaws that you just don't see. Love is blind, after all. To sum up, keep your requests to the items that would prevent you from buying the home. Try to picture being on the other side of the transaction and figure out what you would think was 'reasonable'. Example- AC is not in working order. It is reasonable to ask the seller get AC to be in good working condition. It is not reasonable to expect the seller to replace the AC if they can get the existing unit working properly. |

David and Amanda BlantonMake the Wise Move! Categories

All

Archives

May 2016

Categories

All

|

RSS Feed

RSS Feed